Introduction

A small, though important, set of postsecondary programs have largely escaped the notice of policymakers and researchers: short-term vocational programs lasting between 300-599 clockhours. These short programs are not currently eligible for Pell Grants, but can access federal student loans under the Higher Education Act. We draw on information obtained through a Freedom of Information Act (FOIA) request from the Department of Education to generate counts of programs, basic statistics, and some measures of student outcomes for these short-term postsecondary programs participating in student loan programs. Our data include all short-term programs (lasting 300-599 clockhours over a minimum of 10 weeks) that applied to participate in federal student-loan programs between 2010 and 2019 under Section 481(b)(2) of the Higher Education Act of 1965 (20 U.S.C. 1088(b)(2)).

These programs are understudied in the literature and are not separately identifiable in most public government datasets. In this report, we document the size and scope of these programs, discuss current policies designed to ensure program quality, and explore the implications of alternative accountability policies that regulators might consider.

We find that, as of 2019, there are about 103 programs under 600 clockhours for which students can take out federal student loans, down from 730 such programs in 2010. Seventy percent of the programs participating are offered by for-profit institutions and nearly half are cosmetology programs. Despite reporting high completion and job-placement rates, we find that post-college earnings for students graduating from these programs are quite low—averaging about $24,000 per year, or $12 per hour for a full-time worker.

Current policies offer little in the way of accountability for these short-term programs. The main requirement for participation in loan programs is known as the 70-70 rule, requiring that programs have self-reported completion and job-placement rates of 70% each when they first apply. No standard definition or guidance for job-placement calculations exist, so institutions interpret the rule themselves and report their own figures. As we show below, all approved short-term loan programs report very high self-reported completion and job-placement rates—many well above 70%. We further show that job-placement rates are not correlated with post-completion student earnings.

“Despite reporting high completion and job-placement rates, we find that post-college earnings for students graduating from [short-term] programs are quite low—averaging about $24,000 per year.”

Due to the manipulability of job-placement rates in particular, the 70-70 rule may be inadequate to protect students and taxpayers from low-performing programs. In 2014, the Obama administration enacted the Gainful Employment (GE) rule that would have held these programs—and many others—accountable for debt-to-earnings rates of graduates. The rule was rescinded by the Trump administration before it was implemented, but data on earnings and debt were released. We examine these data and the implications of the GE rule had it been applied to these short-term programs. We find that, despite the very low earnings, short-term programs fare well on debt-to-earnings measures under the Gainful Employment rule due to low borrowing. On average, students in these programs borrow just $750. Only 5% of these short-term programs are in the GE warning “zone” and none of them fail debt-to-earnings thresholds.

Finally, we examine how these programs would fare on other potential accountability metrics—some of which have been proposed previously. In particular, we consider using the average earnings of young adults with no college education as a benchmark for post-completion earnings. When we apply our lowest benchmark of $25,000 (roughly the average for high school dropouts and about 200% of poverty in 2019), more than half of these short-term programs fail. Nearly all failing programs (96%) are in for-profit institutions—many of them in cosmetology and massage.

“It is not clear that [short-term programs] warrant taxpayer support and student debt.”

Our results have implications for regulatory policy surrounding access to loans for these very short vocational programs, and they can inform current proposals to expand access to Pell Grants for similar short-term programs. Although the short-term programs we study have relatively low debt and require only a short time investment, their earnings outcomes are concerning. It is not clear that they warrant taxpayer support and student debt. If these programs continue to participate in federal student-loan programs, we suggest that, at a minimum, policymakers consider adding a high school benchmark on top of GE metrics for any short-term program accessing federal student aid. We further suggest that access to short-term Pell Grants—if implemented—should be limited to public sector programs.

What We Know About Short-Term Programs Accessing Loans

Short-term programs under 600 clockhours are not eligible to participate in the Pell Grant program, but may access federal student loans if they submit an application and gain approval from the Department of Education. A key requirement for approval is the so-called 70-70 rule, requiring that programs have self-reported completion and job-placement rates of 70% each. No standard definition or guidance for job-placement calculations exist, so institutions must track their own graduates and interpret the rule themselves, subject to being verified by an auditor of their choice.

Under the Obama administration, GE regulations were proposed to hold these programs and others—including all for-profit programs and non-degree programs in public and nonprofit institutions—accountable for student outcomes. Programs would lose access to federal student aid if they could not meet certain debt-to-earnings rates. Specifically, programs would fail with annual debt-to-earnings greater than 12% and discretionary debt-to-earnings greater than 30%. They would be in a warning “zone” in a range of 8-12% annual debt-to-earnings or 20-30% discretionary debt-to-earnings. The rule was rescinded by the Trump administration in 2019—before it was fully implemented.

To codify and strengthen accountability for these programs, efforts to reauthorize the Higher Education Act included reinstating GE as well as new proposals based on high school earnings benchmarks. For example, the College Affordability Act (H.R. 4674) put forward by House Democrats in 2019 proposed allowing Pell Grants to be used for short-term programs (lasting 8-15 weeks) in public and nonprofit institutions. It also redefined the rules determining eligibility for short-term programs in all sectors that currently access federal student loans.

In addition to meeting debt-to-earnings thresholds under the GE standards, the College Affordability Act proposed that programs between 300-599 clock hours would need to meet a high school earnings benchmark. Specifically, the proposal required programs to show that the higher of the mean or median earnings of graduates were higher than the national average or (if justified) a state or local average for students with just a high school diploma. Similarly, Pell Grant eligibility for short-term public and nonprofit programs in the College Affordability Act would need to meet “anticipated earnings” benchmarks agreed to by industry or sector partnerships, with the requirement that anticipated earnings be higher than local or national averages for individuals with only a high school diploma.

We examine all three levels of accountability here: the current 70-70 rule, GE regulations, and potential high school benchmarks that could be used to supplement the other metrics.

“Students attending short-term programs tend to be disadvantaged and may be vulnerable to predatory practices, based on limited prior research.”

Students attending short-term programs tend to be disadvantaged and may be vulnerable to predatory practices, based on the limited prior research on these programs. Ositelu, McCann, and Laitinen (2021) report on the many gaps in our understanding of short-term programs. They urge caution as policymakers consider expansions of short-term programs that could leave students of color, in particular, with high debt and little gain. Focusing on past policies surrounding short-term credentials, Whistle (2021) finds that the non-targeted and non-outcomes-based financing of these programs results in worse outcomes for low-income students and students of color. Ositelu (2021) draws on the Adult Training and Education Survey to study short-term programs lasting 15 weeks or less; she finds that half of working adults with a short-term credential were making poverty-level wages in 2016.

Analyzing Outcomes for Short-Term Programs Accessing Loans

Through a FOIA request, we obtained the Education Department’s data on short-term programs accessing loans. The agency collects self-reported completion-rate and placement-rate data for these short-term programs when they apply for the first time or seek re-certification for access to loan programs.1 This data also include basic information on the number of eligible programs, institutions, field of study, program length, and accreditation.

We have information on all programs between 300-599 clock hours lasting at least 10 weeks that applied to participate in federal student-loan programs or were recertified between 2010 and 2019. These programs are offered in 452 institutions and provide about 880 different programs over this period. We drop 27 programs in foreign institutions. Self-reported completion and placement rates under the 70-70 rule are provided for about 476 programs.

We supplement these data with data from the 2017 release of the GE program-level data to assess post-college earnings and how these programs would fare on GE debt-to-earnings metrics. The GE data contain debt-to-earnings rates, debt, and three-year mean and median earnings measures of graduates for programs that were operating between 2010 and 2012. Our FOIA data contain more than 700 short-term programs operating during this time frame, but only 73 report data under GE. The reasons for the mismatch are unclear, but could be due to the small size of many of these programs, as GE does not report outcomes for programs with less than 30 graduates over three years.

Finally, to explore additional proposed accountability metrics, we consider three earnings benchmarks that we classify simply as “low,” “medium,” and “high.” Our most conservative low estimate is just $25,000. This baseline was previously used by the Department of Education in the first release of the College Scorecard in 2013-14 to calculate the percentage of students in each postsecondary institution that make more than a high school graduate. In explaining the use of this benchmark, the College Scorecard notes, “The $25,000 threshold was chosen since it approximately corresponds to the median wage of workers age 25 to 34 with a high-school degree only.” The $25,000 figure is simple, straightforward, and serves as a lower-bound relative to other earnings benchmarks. Updating this statistic with 2019 earnings data, 25-34 year-olds with only a high school diploma only earned an average of $34,867, and, coincidentally, those in the same age range who did not even complete high school had median earnings of $25,536 in 2019. Accordingly, we refer to the low benchmark as approximating high school dropouts’ earnings through the remainder of the report. Moreover, $25,000 roughly corresponds to 200% of the federal poverty line in 2019 for a single person living alone at $24,980. We propose $25,000 as a simple lower bound for this analysis and for policy, but our results would be similar using these alternate benchmarks.

To gain a more relevant representation of current earnings for young students who have completed a high school education, our medium estimate is based on average earnings of $32,787 annually. This reflects the Census Bureau’s calculation of mean earnings of workers who graduated high school in the 18-24 age group who “usually worked 35 hours or more per week for 50 weeks or more during the preceding calendar year” in 2019. Finally, our high estimate is based on all year-round, full-time workers over the age of 18 with a high school diploma. Note that this estimate intentionally includes workers over the age of 25 and does not include those who are unemployed, making it an upper bound at $47,833 per year.

How Many Short-Term Programs Access Student Loans?

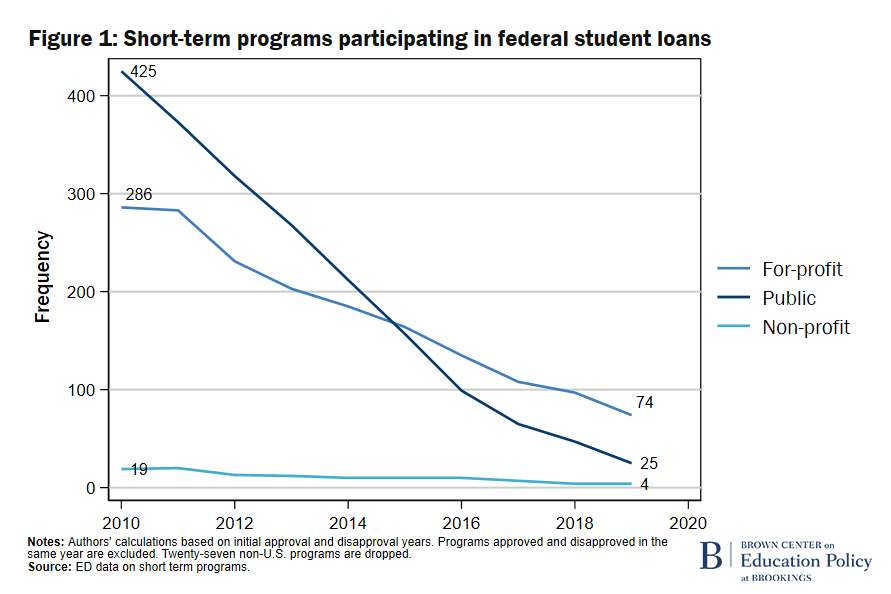

We begin with simple counts of programs lasting between 300-599 clockhours that applied to participate in federal student-loan programs. Figure 1 plots the total number of 300-599 clockhour programs participating in student loan programs each year by sector, regardless of approval date. Most evident is the steep decline in the total number of programs participating over time. In 2010, 730 programs participated. As of our latest complete year of data in 2019, there were just 103 programs participating. The number of public sector programs has plummeted most dramatically, dropping from 425 to 25.

More research is needed to understand the reasons behind the decline in Figure 1, but information on approvals and disapprovals is informative. Figure 2 reports patterns of overall applications, approvals, and disapprovals each year. The number of total applications and new approvals peaked in 2013 with about 48 new programs allowed to participate in federal loan programs that year. Less than half of new applicants are typically approved in any given year. Disapprovals were highest in 2011 and 2016 at around 95 programs. The total number of applications has declined over the last four years, while the number of approvals has held steady, around 15 or so new programs added each year.

The Department of Education data also provide some insight into the reasons for disapproval. The largest category of disapprovals is for programs that “are not long enough” and presumably do not meet the minimum 300 clockhours or 10-week length. In most years, the second-most popular reason for disapproval is not meeting the 70-70 requirement. Interestingly, in 2015, one program was denied for the stated reason of “not leading to gainful employment,” but the definition of this term was not clear and the GE rule was never officially implemented. It is not entirely clear as to why exceedingly short programs or those that do not meet the 70-70 requirements would apply.

What Types of Short-Term Programs are Accessing Loans?

Table 1 reports some descriptive statistics for the 103 short-term programs that are currently participating in federal student-loan programs (as of 2019). Seventy percent of these programs are in for-profit colleges. Less than a quarter of programs are in public institutions, and just 4% are in nonprofits. Cosmetology programs account for nearly half (46%) of all approved short-term programs, but since these are very short programs, they likely reflect programs in sub-fields such as nail technicians and aestheticians, rather than licensed cosmetologists. Welding, truck driving, phlebotomy (drawing blood), and culinary programs round out the top five fields, but each represents less than 8% of the total. Programs are fairly evenly distributed geographically, with Pennsylvania, Florida, and Texas topping the list.

| Table 1: Short-Term Programs Participating in Loan Programs, 2019 | ||

| Number | ||

| Total Number of Programs | 103 | |

| Sectors | ||

| For-profit | 74 | |

| Public | 25 | |

| Nonprofit | 4 | |

| Top 5 Programs | ||

| Cosmetology | 47 | |

| Welding | 8 | |

| Commercial Vehicle Operation | 8 | |

| Phlebotomy | 6 | |

| Cooking & Related Culinary Arts | 3 | |

| Top 6 States | ||

| Pennsylvania | 16 | |

| Florida | 15 | |

| Texas | 11 | |

| New York | 8 | |

| Ohio | 7 | |

| New Jersey | 7 | |

|

Source: Authors tabulations of Education Department data on short-term loan programs. Notes: Top 5 programs lists the fields with the most programs participating in loan programs in 2019. Programs are grouped by the following 4-digit CIP codes: Cosmetology-1204, Welding-4805, Commercial Vehicle Operation-4902, Phlebotomy-5110, Cooking & Related Culinary Arts-1205. Top 6 states lists the states with the most short-term programs participating in loan programs in 2019. A total of 59 schools had at least one program approved for loans in 2019. |

||

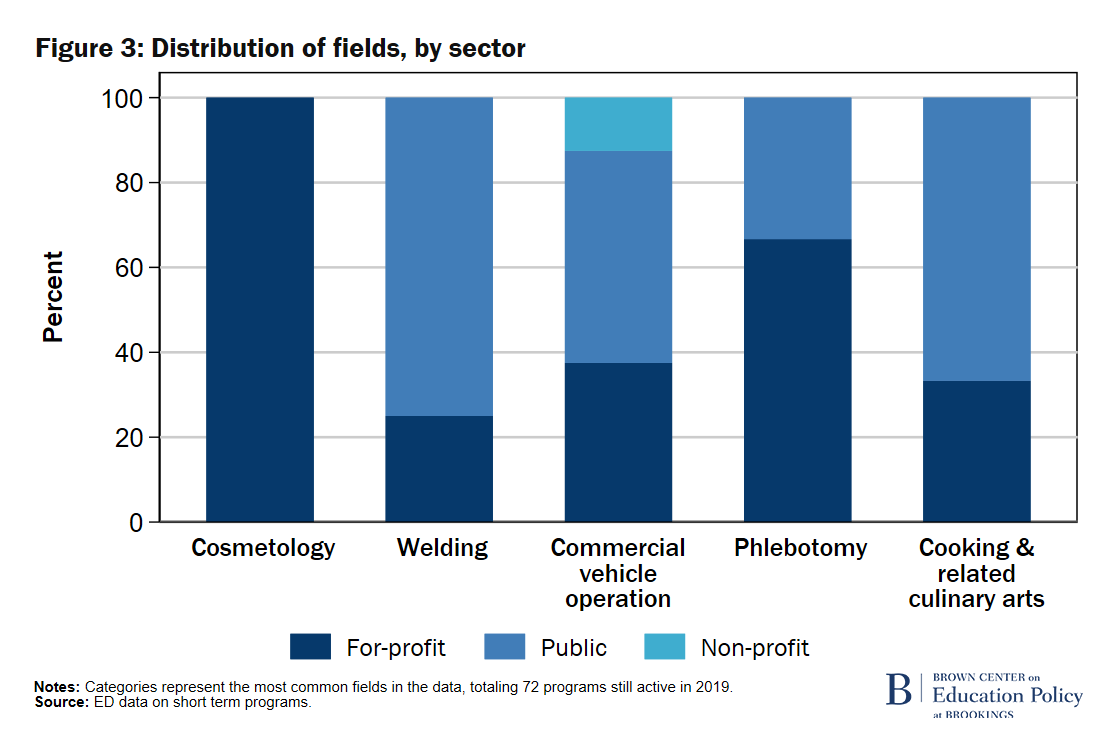

Fields of study differ substantially across sectors. As shown in Figure 3, cosmetology programs take place entirely in for-profit institutions, while welding and culinary-arts programs are disproportionately offered by public institutions, although the numbers of programs are quite small. Nonetheless, these differences by field inform patterns by sector and suggest important differences in student demographics.

Table 2 reports some additional metrics included in the Department of Education data. Notably, average clockhours are quite low, just 367, while the average number of weeks is 17. Most institutions have just one short-term program that accesses federal loans; the mean is 1.7 and the max is three. Many programs have been approved for several years—one as long as 33 years—but the average is about 9 years.

| Table 2: Descriptive Statistics for Short-Term Programs, 2019 | |||

| Mean | Min. | Max. | |

| Number of Programs Offered per Institution | 1.2 | 1 | 3 |

| Number of Years Program Approved | 9 | 0 | 33 |

| Clockhours | 368 | 96 | 563 |

| Number of Weeks | 17 | 10 | 47 |

| Self-Reported Completion Rate | 93 | 70 | 100 |

| Self-Reported Job Placement Rate | 87 | 70 | 100 |

| Total Programs | 103 | ||

|

Source: Authors tabulations of Education Department data on short-term loan programs. Notes: A program approved for zero years was approved to participate in loan programs in 2019. Self-reported completion and job-placement rates are averaged over all years a program reported them in Education Department data. One program had clockhours below 300, listing 96 hours and 36 weeks. |

|||

How Do Short-Term Programs Perform on Outcomes-Based Accountability Measures?

The 70-70 rule

The most interesting information included in the Department of Education data are the self-reported outcome measures under the 70-70 rule. For these approved programs, in Table 2 we can see that all 103 meet the 70% threshold for completion and job placement with the minimum listed as 70 for each. However, the average self-reported completion rate is a high 93% and the self-reported job-placement rate is 87%.

The Gainful Employment rule

We next merge the data with the GE data released in 2017 to measure student earnings and assess how these institutions would fare if the GE rule had been implemented. As noted previously, only 73 short-term programs were successfully matched to the GE data. These are likely to be larger programs and potentially more-established programs than those that were unmatched—that is, they would be positively selected—so we consider our earnings analyses for these merged groups to be optimistic upper bounds of what we might expect if the full set of short-term programs were included. We also recommend that—if GE is reinstated—policymakers consider lowering the threshold number of students needed for inclusion for GE to be effective in holding these types of programs accountable for student outcomes.

Nonetheless, in Table 3 we report how our 73 matched programs fared on GE metrics. The average of the “highest of mean or median earnings” suggests that graduates of these programs have earnings of about $23,800 per year. The mean of the mean is only slightly lower at $23,500. Median annual loan payments are low, averaging $750 with a maximum of $2,782. These low debt measures keep debt-to-earnings annual rates quite low, with annual rates averaging 3.5% and topping out at 9.6% (for comparison, the threshold for failure is 12%). In contrast, discretionary debt-to-earnings rates are quite high, averaging 52% (the failure threshold based on discretionary earnings is 30%). We observe official GE program status—based on failing both the discretionary and annual metrics—in the lower panel: 95% of short-term programs pass and just 5% are in the warning “zone,” with none failing.

| Table 3: Gainful Employment Outcomes for Short-Term Programs | |||

| Mean | Min. | Max. | |

| Highest of Mean or Median Earnings | $23,830 | $8,646 | $80,672 |

| Mean Earnings | $23,533 | $8,646 | $80,672 |

| Median Earnings | $21,768 | $3,846 | $74,718 |

| Annual Debt Payments | $750 | $0 | $2,782 |

| Debt to Earnings Annual Rate | 3.5% | 0.0% | 9.6% |

| Debt to Earnings Discretionary Income Rate | 52.5% | 0.0% | 170.1% |

| Official GE Program Status | |||

| Percent Passing | 94.5% | ||

| Percent in Warning “Zone” | 5.5% | ||

| Percent Failing | 0 | ||

| Total Programs matched with GE Data | 73 | ||

|

Source: Education Department data on short-term loan programs merged with GE data. Notes: Earnings and debt are in 2019$ (USD). |

|||

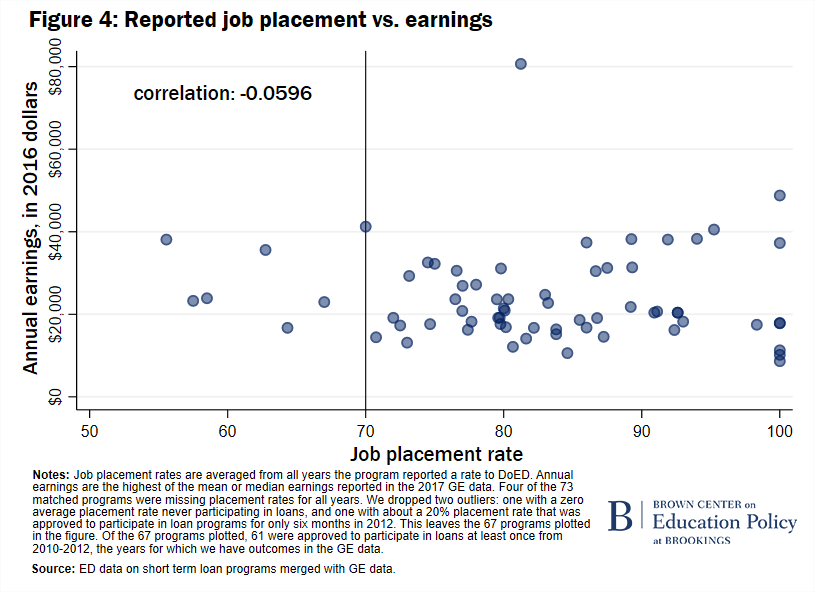

One question arising in policy debates is the reliability of job-placement rates for accountability. Since there is no standard definition, institutions can interpret job placement loosely and, in the case of short-term programs, they self-report them. To better understand the relationship between more reliable earnings measures (based on Social Security Administration data) and job placement, we plot the two values for the set of matched short-term programs in Figure 4. It is obvious from a glance that there is no correlation between the two measures. The calculated correlation coefficient is only -0.0596, with the opposite sign of what we would expect if both were indicative of quality. Thus, it is clear that job placement is a poor proxy for earnings outcomes among these programs. Moreover, Figure 4 shows that most short-term programs have very low earnings, with one obvious outlier around $80,000.

A high school earnings benchmark

To assess a proposed third layer of accountability, we examine various high school earnings metrics. In contrast to debt-to-earnings, the application of a high school earnings metric to assess student outcomes for these programs yields disappointing—but perhaps not surprising—results; these are presented in the first column of Table 4. Based on the lowest high school earnings benchmark ($25,000), 70% of the merged short-term programs fail this metric. That is, less than a third (30%) of the short-term programs yield higher earnings than a 25-34 year-old high school dropout. The medium metric of $32,787 based on high school graduates would yield failures of 84% of our sample. Using the highest metric of $47,833, only two programs of the 73 would pass, yielding a 97% failure rate.

| Table 4: Comparing Earnings Metrics to Gainful Employment Status for Short-Term Programs | |||

| Total failing benchmark (percent of total) | Official GE Status | ||

| Pass | Warning “Zone” | ||

| Low Earnings Benchmark ($25,000) | 51 (69.9%) | 47 | 4 |

| Percent of GE Category Failing on Earnings | – | 68.1% | 100% |

| Med. Earnings Benchmark ($32,787) | 61 (83.6%) | 57 | 4 |

| Percent of GE Category Failing on Earnings | – | 82.6% | 100% |

| High Earnings Benchmark ($47,833) | 71 (97.3%) | 67 | 4 |

| Percent of GE Category Failing on Earnings | – | 97.1% | 100% |

| Total short-term programs | 73 (100%) | 69 | 4 |

|

Source: Education Department data on short-term programs merged with GE data. Notes: Counts of programs that failed each high school earnings metric compared to the counts of programs in Pass or Warning “Zone” GE status. Percent of GE Category Failing calculates the percentage of programs that pass GE (or in the Warning “Zone”) that fail each high school earnings benchmark. GE earnings data are adjusted from 2016$ to 2019$ (USD). |

|||

The two right-most columns of Table 4 break out the programs that fail each earnings benchmark into passing/failing the debt-to-earning metrics under the GE rule to compare these different accountability approaches. Of the 51 programs that fail the lowest high school metric, 47 pass GE and 4 are in the warning “zone.” Looking at it a different way in the second row, of those that pass GE, 68% would still fail our lowest high school earnings metric. If there is an expectation that postsecondary programs receiving federal student aid should result in earnings greater than high school, even the lowest high school earnings metric—added to GE—could provide an additional measure of accountability.

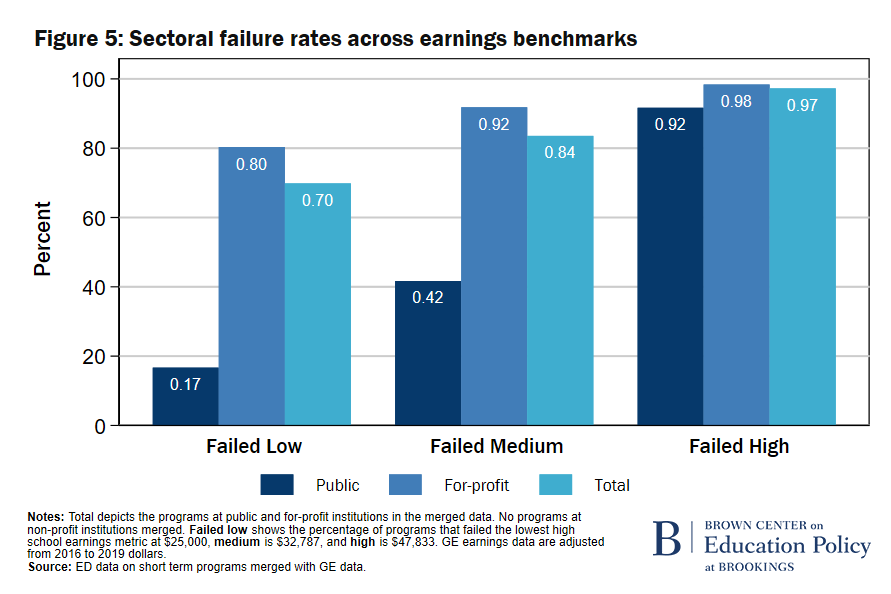

Figure 5 presents failure rates by sector. Forty-nine for-profit programs (80%) fail the lowest high school metric, compared to just two public programs (17%). Calculated across all failing programs on our lowest earnings benchmark, 96% come from the for-profit sector. The difference in failure rate between sectors narrows with the medium and high earnings benchmarks, though for-profits fail at higher rates across all levels.

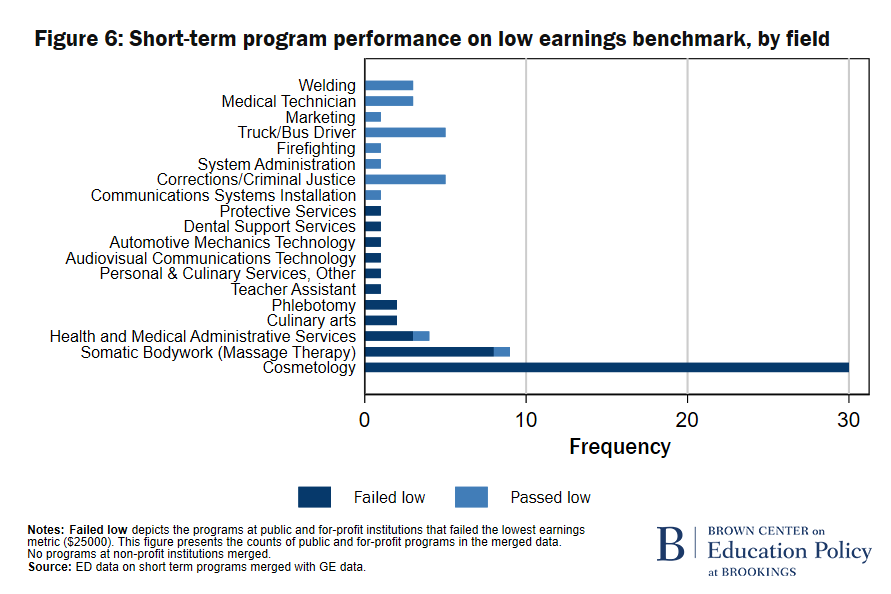

As noted above, fields of study are not evenly distributed across sectors. Figure 6 counts passing and failing programs (using the lowest earnings benchmark) by field of study. Cosmetology is the largest field of study in the data, and with all cosmetology programs reporting less than $25,000, they make up nearly two-thirds of all failing programs. Massage therapy is next, with all but one program failing to meet the low earnings benchmarks, accounting for 17% of all failing programs. Among the four health administration programs in our data, three fail. All other fields with failures have just one program in the data, so we view these are merely suggestive. Fields with more than one program in which all programs pass the lowest high school benchmark include criminal justice, truck driving, medical technicians, and welding.

More research is needed to better understand these patterns, but it is possible that gender differences across fields could be contributing to these differential outcomes as passing fields appear more heavily male and failing fields are more heavily female. Disparities may also be related to employment trends and the way earnings are reported in different fields. For example, the main cosmetology trade association, the American Association of Cosmetology Schools, has been successful in its legal efforts to gain exceptions to earnings-based accountability rules due to the prevalence of underreported tipped income in the field. Whether or not underreporting drives performance on these metrics is the subject of ongoing research.

Implications for Policy

In the last decade, about 880 short-term programs under 600 clockhours applied to participate in federal student-loan programs, and about 500 of these programs were approved in this period. Including approvals from earlier years, in 2010, about 730 short-term programs participated in federal student-loan programs, but this figure has declined over time. In 2019, the most recent year of our data, 103 programs participated. Seventy percent of these programs take place in for-profit institutions and 47% are cosmetology programs.

To gain eligibility, programs must meet the 70-70 criteria regarding completion and job-placement rates. Among approved programs, completion and job-placement averages are high, but can be misleading. In particular, job placement is not clearly defined in statute, allowing nearly any job to count as in-field. For example, a student who attended a cosmetology program may be considered placed “in-field” if they are working as a cashier at a salon.

“[J]ob placement is not clearly defined in statute, allowing nearly any job to count as in-field. For example, a student who attended a cosmetology program may be considered placed ‘in-field’ if they are working as a cashier at a salon.”

Earnings are more reliable metrics to assess quality in postsecondary programs. Not surprisingly, we find that earnings of graduates are not correlated with reported job-placement rates. The average earnings for these programs is about $24,000, or about $12 per hour for a full-time worker. Average debt is roughly $750.

In 2014, the Obama administration enacted the GE rule to add an additional layer of accountability for a number of different programs, including the short-term programs we investigate here. The rule was rescinded before it was fully implemented, but notably, very few of these short-term programs appear in the GE data, suggesting that they fell below the reporting thresholds based on low number of graduates. Of the 73 programs we observe in the GE data, 95% pass the GE debt-to-earnings thresholds.

If these programs are to continue to access student loans, we support the creation of an additional earnings benchmark to be used in conjunction with GE for these short-term programs to ensure student protection. Such a measure could be based on a comparison of a program’s earnings to a benchmark based on the average earnings of young people who graduate high school but do not attend college. Our data show that 70% of the short-term programs we study would fail even the lowest justifiable benchmark of just $25,000 per year based on the average earnings of high school dropouts. Virtually all (96%) of these failing programs are in for-profit institutions, at least in part due to the prevalence of (failing) cosmetology and massage programs in the sector. Programs in male-dominated fields, such as welding and truck driving, appear to perform better against these benchmarks. Higher benchmarks—such as our medium benchmark of $32,787 based on high school graduates’ earnings—might be more easily justified for policy, as postsecondary institutions should, at least in theory, enroll high school graduates and generate more earnings for students than high school alone. Any such earnings thresholds could easily be adjusted to account for differences in wage levels in states or local areas and could flexibly adjust to changing labor market conditions. Research in progress examines these types of alternate thresholds for a broader set of programs.

“Policymakers should consider changes to the 70-70 rule that strengthen accountability and avoid relying on an easily manipulated job-placement measure.”

More research is needed to adjust for student selection in assessing outcomes and to explore the role of tipped income in earnings measures, but our descriptive analyses suggest that concerns about the value of these short-term programs for students is justified. Policymakers should consider changes to the 70-70 rule that strengthen accountability and avoid relying on an easily manipulated job-placement measure. Policymakers should also ensure that all short-term programs are subject to GE regulations, perhaps lowering the number of graduates for which exemptions apply.

In addition to GE, we support imposing a high school earnings benchmark or similar threshold earnings measure for short-term programs accessing student loans, as well as for any expansion of the Pell Grant program to short-term programs. In light of these results and other research on sectoral differences in student outcomes in short-term programs, we further suggest that any access to short-term Pell Grants be limited to public sector programs.

"term" - Google News

July 23, 2021 at 12:04AM

https://ift.tt/3rt0sZT

Quick college credentials: Student outcomes and accountability policy for short-term programs - Brookings Institution

"term" - Google News

https://ift.tt/35lXs52

https://ift.tt/2L1ho5r

Bagikan Berita Ini

0 Response to "Quick college credentials: Student outcomes and accountability policy for short-term programs - Brookings Institution"

Post a Comment